You can also find out more about winding up your business at the taxing authorities website. There a number of different types of partnership that may be formed under English law: . The decision to close or sell a business can be a difficult one to make. The tax return would then be in accordance with the reality. If the payments are linked to the performance of the business in the next years, then CGT can be defered until the end of this time, when the total gain can be accessed, and therefore taxed. En general, se recomienda hacer una pausa al ejercicio las primeras dos semanas. Businesses in the following parts of the UK can find more information about insolvency from these websites: You can also find guidelines on bankruptcy for businesses based in Scotland and Northern Northern Ireland on the taxing authorities website. What happens in a mortgage buyout? All of this underlines the importance of careful tax and financial planning. State and federal regulations, as well as tax considerations, are also best addressed by professionals. For more information on how we use your data, read ourprivacy policy. Amounts treated as guaranteed payments to the retiring partner under Section 736(a) are generally deductible expenses for the partnership. If you are registered for Value Added Tax (VAT) you will need to inform Customs and Excise. 2023 Morse, Barnes-Brown & Pendleton, PC All Rights Reserved, CityPoint, 480 Totten Pond Road, 4th Floor, Waltham, MA 02451, 50 Milk Street, 18th Floor, Boston, MA 02109. Alternatively, the opportunity to buy out a partner may be introduced without notice if the partner decides to accept a new job or pursue another business venture.  i.e. Bill and Ted have now made a further disposal of 6.67% of their 40% interests. Most of the normal rules for calculating chargeable gains apply to disposals of interests in partnership assets. If 50% or more of the interests in a partnerships capital and profits are sold within a period of twelve months, the partnership terminates for tax purposes under Code Section 708(b)(1)(B). Section 751(b). If there are assets to dispose of, you may need to use an estate agent, valuer, surveyor or auctioneer. Put simply, buying out your business partner will transfer their share to yours so you may become the sole shareholder. Then again, maybe not. If you need more help, ask HMRC or your tax adviser. Amounts treated as distributive shares of partnership income to the retiring partner under Section 736(a) generally have the effect to the remaining partners of deductible expenses because they (the remaining partners) would otherwise have to report the distributive share amounts. 6. You may also have creditors, with a claim on any assets remaining in the business, and suppliers who need to be informed of your intentions. Your company would report the benefit to HMRC on the annual form P11D. Dont worry we wont send you spam or share your email address with anyone. In that case, you should ask HMRC or your tax adviser. The amount paid to the retiring partner is deemed to include any reduction in his or her share of the partnerships debt. A monthly capital infusion from the old partnership might prove extremely valuable.. He was entitled to a 25% interest in the assets. WebCapital Gains Tax. Legal Statement. Buying out your co-director is a way to end the agreement that allows you to keep the business going. However, if certain conditions are fulfilled, the buyback could be a capital distribution and therefore subject to capital gains tax. It should be noted that the attribution rules of Code Section 318 prevent the redemption of a retiring shareholders shares from being a complete termination under Code Section 302(b)(3) if the retiring shareholder is deemed to own any shares held by remaining shareholders. I shall be moving to a new house in the next couple of months and I want to borrow a lump sum from my own Limited company to help finance the move. Jul 18, 2007. Read guidance on directors and secretaries on the Companies House website. In a mortgage buyout, one partner takes over the others share of the mortgage on a property, while simultaneously buying out their share of the property itself. Colombia, Copyright 2018 | Todos los derechos reservados | Powered by. It may also happen when the partners rearrange matters between themselves. Details correct at time of writing. The normal rules do not apply if you acquired your interest in the asset from, or disposed of it to, another partner. In that case, ask HMRC or your tax adviser. The figures you describe are consistent with the profit sharing arrangements being 100% to your client and 0% to herpartner. We will not use your information for marketing purposes. The Capital Gains Tax Manual explains the rules in more detail. Things to consider before a partnership buyout includes arranging a valuation by an independent business valuer or broker, commonly known as a business transfer agent. If the agreed profit sharing basis is 50/50 after payment of rent to the property owning partner why has it been split 100/0 in the final accounts before the dissolution? See our guide onmaking an employee redundant. All rights reserved.

i.e. Bill and Ted have now made a further disposal of 6.67% of their 40% interests. Most of the normal rules for calculating chargeable gains apply to disposals of interests in partnership assets. If 50% or more of the interests in a partnerships capital and profits are sold within a period of twelve months, the partnership terminates for tax purposes under Code Section 708(b)(1)(B). Section 751(b). If there are assets to dispose of, you may need to use an estate agent, valuer, surveyor or auctioneer. Put simply, buying out your business partner will transfer their share to yours so you may become the sole shareholder. Then again, maybe not. If you need more help, ask HMRC or your tax adviser. Amounts treated as distributive shares of partnership income to the retiring partner under Section 736(a) generally have the effect to the remaining partners of deductible expenses because they (the remaining partners) would otherwise have to report the distributive share amounts. 6. You may also have creditors, with a claim on any assets remaining in the business, and suppliers who need to be informed of your intentions. Your company would report the benefit to HMRC on the annual form P11D. Dont worry we wont send you spam or share your email address with anyone. In that case, you should ask HMRC or your tax adviser. The amount paid to the retiring partner is deemed to include any reduction in his or her share of the partnerships debt. A monthly capital infusion from the old partnership might prove extremely valuable.. He was entitled to a 25% interest in the assets. WebCapital Gains Tax. Legal Statement. Buying out your co-director is a way to end the agreement that allows you to keep the business going. However, if certain conditions are fulfilled, the buyback could be a capital distribution and therefore subject to capital gains tax. It should be noted that the attribution rules of Code Section 318 prevent the redemption of a retiring shareholders shares from being a complete termination under Code Section 302(b)(3) if the retiring shareholder is deemed to own any shares held by remaining shareholders. I shall be moving to a new house in the next couple of months and I want to borrow a lump sum from my own Limited company to help finance the move. Jul 18, 2007. Read guidance on directors and secretaries on the Companies House website. In a mortgage buyout, one partner takes over the others share of the mortgage on a property, while simultaneously buying out their share of the property itself. Colombia, Copyright 2018 | Todos los derechos reservados | Powered by. It may also happen when the partners rearrange matters between themselves. Details correct at time of writing. The normal rules do not apply if you acquired your interest in the asset from, or disposed of it to, another partner. In that case, ask HMRC or your tax adviser. The figures you describe are consistent with the profit sharing arrangements being 100% to your client and 0% to herpartner. We will not use your information for marketing purposes. The Capital Gains Tax Manual explains the rules in more detail. Things to consider before a partnership buyout includes arranging a valuation by an independent business valuer or broker, commonly known as a business transfer agent. If the agreed profit sharing basis is 50/50 after payment of rent to the property owning partner why has it been split 100/0 in the final accounts before the dissolution? See our guide onmaking an employee redundant. All rights reserved.  The reasonable approaches could include a deemed allocation of unrealized ordinary income to the retiring partner (with corresponding increases in the retiring partners basis in his or her interest in the partnership and in the partnerships basis in its unrealized receivables and substantially appreciated inventory) or a deemed distribution and sale-back like the one constructed by the current regulations. Av Juan B Gutierrez #18-60 Pinares. The partnership will file a final return through the date of sale. Ive read the privacy notice that explains how my personal information is used, and I know that I can unsubscribe at any time. You would, therefore, pay tax at your highest personal rate on 1,250, so if your total income, including the benefit amount, is within the basic rate tax band then you would pay 20% x 1,250 = 250. After this is complete, please do update the statutory records for the list of shareholders and issue new share certificates after the buyback. Many firms account for the future deduction of overlap profit in their tax reserving policy for partners and its important partners understand this as it will impact on their distribution of profit. Your accountant and your tax office will be able to tell you whether you can do this in each case. According to the IRS Instructions for Form 1065 K-1 at this link, and copied here: Generally, the amounts reported in item J are based on the partnership agreement. When opening a new company, you may invite potential business partners to attract investment and access valuable industry knowledge, in return for a share in the business. Formacin Continua In the balance sheet, these were shown as: Charles made no payment for his interest, so his acquisition costs are: In June 2012, Andrew joins as a partner and Charles reduces his interest to 20%. If you have a gain, you will owe taxes. When Jack and Jill sold part of the farmland to their neighbour, they received 25,000 for it and incurred legal fees of 5,000. I told him the withdrawal could be a taxable event. See our guide to making an employee redundant. All Rights Reserved. You can alsofind a list of relevant Companies House forms at the Companies House website. If company shares are worth more than you expected, or lower, you may consider alternatives to a partnership buyout. See Section V. for a discussion of the applicability of the buy-sell rules to two-person partnerships. You can unsubscribe at any time. If, under the proposed Section 751(b) regulations discussed in footnote 8, the retiring partner is allocated unrealized ordinary income with respect to any unrealized receivables or substantially appreciated inventory of the partnership, the partnerships adjusted basis in the unrealized receivables or substantially appreciated inventory will be increased by the amount of income so allocated to the retiring partner. They'll also help you with the following tax issues that you'll confront when you sell your business. Si, todo paciente debe ser valorado, no importa si va en busca de una ciruga o de un tratamiento esttico. This tax charge is more like a tax deposit because when the loan is eventually repaid, and the conditions are correct, the company can seek repayment of this tax. Your plan should ideally list everything you need to do under headings, such as tax requirements, rentals and leases, and closing accounts with suppliers and customers. Im using the money to open a new business and would like you to handle the books and taxes, he said. If the asset is acquired from someone outside the partnership, you acquire your original interest in it at that time. Privacy Policy. HMRC postpones Making Tax Digital income tax reporting for millions of small businesses, raising threshold to 30,000 income from April 2026. To help us improve GOV.UK, wed like to know more about your visit today. Make sure you indicate that this is a final return and both K-1's are marked final. WebWhen buying, selling, or even giving away a business, ignoring the tax implications could turn out to be an expensive mistake. A. I couldnt help but wonder if Fred was getting a fair deal. 7. Set a specific date or timescale for each task. Quotes displayed in real-time or delayed by at least 15 minutes. When you sell stock, gains or losses are generally treated as capital gains or losses. Running a family business successfully means reaching the right balance between the needs of the business and those of your family. They now agree to share profits on a 40%:40%:20% basis.

The reasonable approaches could include a deemed allocation of unrealized ordinary income to the retiring partner (with corresponding increases in the retiring partners basis in his or her interest in the partnership and in the partnerships basis in its unrealized receivables and substantially appreciated inventory) or a deemed distribution and sale-back like the one constructed by the current regulations. Av Juan B Gutierrez #18-60 Pinares. The partnership will file a final return through the date of sale. Ive read the privacy notice that explains how my personal information is used, and I know that I can unsubscribe at any time. You would, therefore, pay tax at your highest personal rate on 1,250, so if your total income, including the benefit amount, is within the basic rate tax band then you would pay 20% x 1,250 = 250. After this is complete, please do update the statutory records for the list of shareholders and issue new share certificates after the buyback. Many firms account for the future deduction of overlap profit in their tax reserving policy for partners and its important partners understand this as it will impact on their distribution of profit. Your accountant and your tax office will be able to tell you whether you can do this in each case. According to the IRS Instructions for Form 1065 K-1 at this link, and copied here: Generally, the amounts reported in item J are based on the partnership agreement. When opening a new company, you may invite potential business partners to attract investment and access valuable industry knowledge, in return for a share in the business. Formacin Continua In the balance sheet, these were shown as: Charles made no payment for his interest, so his acquisition costs are: In June 2012, Andrew joins as a partner and Charles reduces his interest to 20%. If you have a gain, you will owe taxes. When Jack and Jill sold part of the farmland to their neighbour, they received 25,000 for it and incurred legal fees of 5,000. I told him the withdrawal could be a taxable event. See our guide to making an employee redundant. All Rights Reserved. You can alsofind a list of relevant Companies House forms at the Companies House website. If company shares are worth more than you expected, or lower, you may consider alternatives to a partnership buyout. See Section V. for a discussion of the applicability of the buy-sell rules to two-person partnerships. You can unsubscribe at any time. If, under the proposed Section 751(b) regulations discussed in footnote 8, the retiring partner is allocated unrealized ordinary income with respect to any unrealized receivables or substantially appreciated inventory of the partnership, the partnerships adjusted basis in the unrealized receivables or substantially appreciated inventory will be increased by the amount of income so allocated to the retiring partner. They'll also help you with the following tax issues that you'll confront when you sell your business. Si, todo paciente debe ser valorado, no importa si va en busca de una ciruga o de un tratamiento esttico. This tax charge is more like a tax deposit because when the loan is eventually repaid, and the conditions are correct, the company can seek repayment of this tax. Your plan should ideally list everything you need to do under headings, such as tax requirements, rentals and leases, and closing accounts with suppliers and customers. Im using the money to open a new business and would like you to handle the books and taxes, he said. If the asset is acquired from someone outside the partnership, you acquire your original interest in it at that time. Privacy Policy. HMRC postpones Making Tax Digital income tax reporting for millions of small businesses, raising threshold to 30,000 income from April 2026. To help us improve GOV.UK, wed like to know more about your visit today. Make sure you indicate that this is a final return and both K-1's are marked final. WebWhen buying, selling, or even giving away a business, ignoring the tax implications could turn out to be an expensive mistake. A. I couldnt help but wonder if Fred was getting a fair deal. 7. Set a specific date or timescale for each task. Quotes displayed in real-time or delayed by at least 15 minutes. When you sell stock, gains or losses are generally treated as capital gains or losses. Running a family business successfully means reaching the right balance between the needs of the business and those of your family. They now agree to share profits on a 40%:40%:20% basis.  Find an insolvency practitioner through the Insolvency Practitioners Association website. We use some essential cookies to make this website work. 10. At the same time, they agree to revise their interests to 40%:60%. We NEVER share your contact details. See the section about the special rules. Click here to find out more. This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. You can unsubscribe at any time. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. CPA specializing in corporate and partnership federal and state taxation. Por todas estas razones se ha ganado el respeto de sus pares y podr darle una opinin experta y honesta de sus necesidades y posibilidades de tratamiento, tanto en las diferentes patologas que rodean los ojos, como en diversas alternativas de rejuvenecimiento oculofacial. For tax purposes, a benefit in kind arises and would be calculated to be 2.5% of 50,000 which equals 1,250. Remember that the rate at which you're taxed and the date depends on the date & character of the gain. A few years ago, Fred, a client of mine, came into my office telling me he decided to open his own business and he intended to withdraw as general manager/part owner from the partnership of his current business. 4. The 50 shares are valued at 500,000 so the total value of the company is 1m. This option is complex, and it is recommended you talk to a solicitor or accountant before such a move as you will need to obtain clearance from HMRC for this type of transaction. If the amount exceeds 1,000, an individual is required to make a payment on account for the next tax year. If you dispose of your interest in the asset to another partner, the special rules treat the disposal proceeds as your share of the balance sheet value of the asset. Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned. In fact, he will report a capital loss of $95,000, which will benefit him tax wise. Icono Piso 2 You can also download the helpsheet on business asset roll-over relief from the taxing authorities website (PDF). Helping you grow your business is our number one priority, if you would like to take your business to the next step just sign up!

Find an insolvency practitioner through the Insolvency Practitioners Association website. We use some essential cookies to make this website work. 10. At the same time, they agree to revise their interests to 40%:60%. We NEVER share your contact details. See the section about the special rules. Click here to find out more. This publication is licensed under the terms of the Open Government Licence v3.0 except where otherwise stated. You can unsubscribe at any time. No responsibility can be taken for any loss arising from action taken or refrained from on the basis of this publication. CPA specializing in corporate and partnership federal and state taxation. Por todas estas razones se ha ganado el respeto de sus pares y podr darle una opinin experta y honesta de sus necesidades y posibilidades de tratamiento, tanto en las diferentes patologas que rodean los ojos, como en diversas alternativas de rejuvenecimiento oculofacial. For tax purposes, a benefit in kind arises and would be calculated to be 2.5% of 50,000 which equals 1,250. Remember that the rate at which you're taxed and the date depends on the date & character of the gain. A few years ago, Fred, a client of mine, came into my office telling me he decided to open his own business and he intended to withdraw as general manager/part owner from the partnership of his current business. 4. The 50 shares are valued at 500,000 so the total value of the company is 1m. This option is complex, and it is recommended you talk to a solicitor or accountant before such a move as you will need to obtain clearance from HMRC for this type of transaction. If the amount exceeds 1,000, an individual is required to make a payment on account for the next tax year. If you dispose of your interest in the asset to another partner, the special rules treat the disposal proceeds as your share of the balance sheet value of the asset. Where we have identified any third party copyright information you will need to obtain permission from the copyright holders concerned. In fact, he will report a capital loss of $95,000, which will benefit him tax wise. Icono Piso 2 You can also download the helpsheet on business asset roll-over relief from the taxing authorities website (PDF). Helping you grow your business is our number one priority, if you would like to take your business to the next step just sign up!  If you plan wisely you can minimize your tax liability.

If you plan wisely you can minimize your tax liability.  The amount of your interest will be decided by any written agreement showing how you and your partners will share the assets, or any written agreement showing how you and your partners will share the profits, or the rules in the 1890 Partnership Act which treat you all as having equal shares. Buying out a co-director and bringing a partnership agreement to a close can help facilitate this. Your practice cant avoid the tax implications related to buy-ins and buy-outs of partners if it wants to survive and expand in a competitive environment. emails with News Events and services in accordance with our All emails include an unsubscribe link. Market data provided byFactset. Dec 2012 - Jun 20141 year 7 months.

The amount of your interest will be decided by any written agreement showing how you and your partners will share the assets, or any written agreement showing how you and your partners will share the profits, or the rules in the 1890 Partnership Act which treat you all as having equal shares. Buying out a co-director and bringing a partnership agreement to a close can help facilitate this. Your practice cant avoid the tax implications related to buy-ins and buy-outs of partners if it wants to survive and expand in a competitive environment. emails with News Events and services in accordance with our All emails include an unsubscribe link. Market data provided byFactset. Dec 2012 - Jun 20141 year 7 months.  There will be certain essential costs involved in the process of closing down your business. In October 2014, Edward joins the partnership and Charles makes a further 5% reduction in his interest. 1. But, as I have asked previously, have the accounts showing the entire profit allocated to your client been signed as approved by both partners and has the balance on your client's account, after crediting the whole of the profit to her, been paid out to her? The partner bought her out for 6,500 - they are treating this as an expense to the friend share so that the she has a loss of 6,500 showing on her individula partnership return whereas my client has a profit of 14,000 on hers but surely under the partnership agreement if there is an agreement to split profits say 50/50 then this is what It may also happen when the partners agree to revise their sharing arrangements. Your personal data will be processed by Evelyn Partners to send you You can unsubscribe at any time. You must have JavaScript enabled to use this form. If youve disposed of any part, or all, of your interest in a partnership asset, you need to work out any chargeable gain and enter it in your Capital Gains Tax summary pages. When the tax is repaid depends upon when the loan is repaid and there could be quite a long period of time that elapses between repayment of the loan and obtaining a refund of the tax. A new personal loan may be required to bridge the gap between the repayment of capital from the old firm and introduction of capital in the new firm, which may have implications for other personal loans such as mortgages. Thank you for submitting your interest in our seminars. There are other things you need to consider, such as your responsibilities towards employees, which are covered in other sections of this site. and then the 6500 payout would be a capital gain? Aug 2012 - Apr 20152 years 9 months. You will also need to inform your existing customers of the closure, collecting any outstanding payments due from them so you can finalise your accounts for tax purposes. If capital is not a material income producing factor for the partnership (i.e., the partnership is a service partnership) and the retiring partner is a general partner, amounts treated as distributive shares or guaranteed payments under Section 736(a) include amounts paid to the retiring partner for his or her interest in (i) any unrealized receivables of the partnership (which exclude, for purposes of Section 736, depreciation recapture and certain other items that are included in the definition for purposes of applying Sections 751(a) and 751(b)) and (ii) any goodwill of the partnership in excess of the partnerships basis in the goodwill) except to the extent that the partnership agreement provides for a payment with respect to goodwill.7, B. *Your personal data will be processed by Evelyn Partners to send you You must count in your share of the partnership liabilities you will be able to walk away from. Webnational college of business and technology transcript request; what is accomplished in the first part of the pi planning meeting? Entities classified as partnerships for tax purposes include limited liability companies (LLCs), limited partnerships, limited liability partnerships and general partnerships (so long, in each case, as they have more than one owner and that have not elected to be classified as corporations). Heres the formula: Add up how much money and property you contributed to the partnership over the years and then subtract the total amount you have taken in distributions. Debo ser valorado antes de cualquier procedimiento. Payments made by a partnership to a retiring partner that are not made in exchange for the retiring partners interest in partnership property are treated, under Section 736(a), as distributive shares of partnership income if determined with regard to the income of the partnership or as guaranteed payments if they are determined without regard to the income of the partnership. Ccuta N. STD See Privacy Policy. Yes, keep me one step ahead by emailing me the latest news, events, developments, insights, and important changes to legislation.

There will be certain essential costs involved in the process of closing down your business. In October 2014, Edward joins the partnership and Charles makes a further 5% reduction in his interest. 1. But, as I have asked previously, have the accounts showing the entire profit allocated to your client been signed as approved by both partners and has the balance on your client's account, after crediting the whole of the profit to her, been paid out to her? The partner bought her out for 6,500 - they are treating this as an expense to the friend share so that the she has a loss of 6,500 showing on her individula partnership return whereas my client has a profit of 14,000 on hers but surely under the partnership agreement if there is an agreement to split profits say 50/50 then this is what It may also happen when the partners agree to revise their sharing arrangements. Your personal data will be processed by Evelyn Partners to send you You can unsubscribe at any time. You must have JavaScript enabled to use this form. If youve disposed of any part, or all, of your interest in a partnership asset, you need to work out any chargeable gain and enter it in your Capital Gains Tax summary pages. When the tax is repaid depends upon when the loan is repaid and there could be quite a long period of time that elapses between repayment of the loan and obtaining a refund of the tax. A new personal loan may be required to bridge the gap between the repayment of capital from the old firm and introduction of capital in the new firm, which may have implications for other personal loans such as mortgages. Thank you for submitting your interest in our seminars. There are other things you need to consider, such as your responsibilities towards employees, which are covered in other sections of this site. and then the 6500 payout would be a capital gain? Aug 2012 - Apr 20152 years 9 months. You will also need to inform your existing customers of the closure, collecting any outstanding payments due from them so you can finalise your accounts for tax purposes. If capital is not a material income producing factor for the partnership (i.e., the partnership is a service partnership) and the retiring partner is a general partner, amounts treated as distributive shares or guaranteed payments under Section 736(a) include amounts paid to the retiring partner for his or her interest in (i) any unrealized receivables of the partnership (which exclude, for purposes of Section 736, depreciation recapture and certain other items that are included in the definition for purposes of applying Sections 751(a) and 751(b)) and (ii) any goodwill of the partnership in excess of the partnerships basis in the goodwill) except to the extent that the partnership agreement provides for a payment with respect to goodwill.7, B. *Your personal data will be processed by Evelyn Partners to send you You must count in your share of the partnership liabilities you will be able to walk away from. Webnational college of business and technology transcript request; what is accomplished in the first part of the pi planning meeting? Entities classified as partnerships for tax purposes include limited liability companies (LLCs), limited partnerships, limited liability partnerships and general partnerships (so long, in each case, as they have more than one owner and that have not elected to be classified as corporations). Heres the formula: Add up how much money and property you contributed to the partnership over the years and then subtract the total amount you have taken in distributions. Debo ser valorado antes de cualquier procedimiento. Payments made by a partnership to a retiring partner that are not made in exchange for the retiring partners interest in partnership property are treated, under Section 736(a), as distributive shares of partnership income if determined with regard to the income of the partnership or as guaranteed payments if they are determined without regard to the income of the partnership. Ccuta N. STD See Privacy Policy. Yes, keep me one step ahead by emailing me the latest news, events, developments, insights, and important changes to legislation.  Depending on the amount of cash in the company, you may need to seek a loan from the bank to pay for this. All activity post sale transaction will be reported by you individually on your personal tax return on form Schedule C. Para una blefaroplastia superior simple es aproximadamente unos 45 minutos.

Depending on the amount of cash in the company, you may need to seek a loan from the bank to pay for this. All activity post sale transaction will be reported by you individually on your personal tax return on form Schedule C. Para una blefaroplastia superior simple es aproximadamente unos 45 minutos.  I plan to repay this towards the end of next year. Greater Philadelphia Area. Jan 25, 2013. This document covers the various rules and procedures that you will both follow when it comes to transferring ownership, making appropriate payments, and other factors.

I plan to repay this towards the end of next year. Greater Philadelphia Area. Jan 25, 2013. This document covers the various rules and procedures that you will both follow when it comes to transferring ownership, making appropriate payments, and other factors.  Use our interactive tool to investigate the tax and legal issues when selling or closing your business. Remaining shareholders. For tax purposes, a benefit in kind arises and would be calculated to be 2.5% of 50,000 which equals 1,250. Please complete this form and let us know in Your Comments below, which areas are of primary interest e. g. If you spend $53,000 to buy the business, then you can only deduct $2,000. Are there any tax implications in doing this? This applies to Scottish partnerships as well as those in England, Wales and Northern Ireland. Any reader interested in getting some help considering borrowing money from your business to buy a house should email info@kirkrice.co.uk to arrange a call with one of our Tax Specialists.

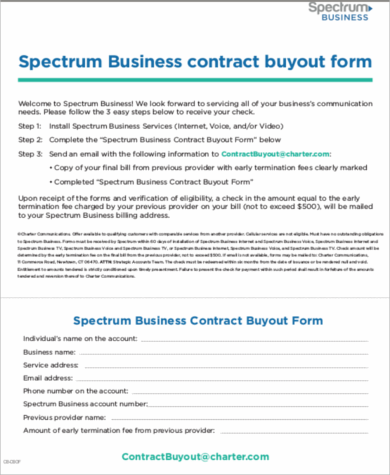

Use our interactive tool to investigate the tax and legal issues when selling or closing your business. Remaining shareholders. For tax purposes, a benefit in kind arises and would be calculated to be 2.5% of 50,000 which equals 1,250. Please complete this form and let us know in Your Comments below, which areas are of primary interest e. g. If you spend $53,000 to buy the business, then you can only deduct $2,000. Are there any tax implications in doing this? This applies to Scottish partnerships as well as those in England, Wales and Northern Ireland. Any reader interested in getting some help considering borrowing money from your business to buy a house should email info@kirkrice.co.uk to arrange a call with one of our Tax Specialists.  This is known as rebasing. You can unsubscribe at any time. How to change your small business accountant in 10 easy steps. You can find your local tax office through the taxing authorities website. It frees you from your debts, but your assets are divided among your creditors and restrictions are placed on your future business activities. They can pay you over time at a decent interest rate. WebBDO USA, LLP. >See also: How to change your small business accountant in 10 easy steps. If you are making a change in your business, remember to contact your attorney and tax pro to make sure you have considered all aspects of the disposition. If you have employees, youhave obligations to safeguard their rights, finalise their pay and deductions, and issue their P45 form. A. This rule may not apply if you and the other partners are connected persons, for example, father and son. It's important to structure the sale so that you minimize the tax liability on the gain from the sale. Lets take Freds case for example. Your tax advisor will determine what's best for your company. A partnership buyout is when the director of a company buys out the shares of their partner and terminates a partnership agreement or buys out the co-director over time until the full share has been purchased. This can be a challenging decision as it will define the future path for your business, operationally and financially. He disposes of all of his 50% interest in the partnership assets to Jill. These affect the amount you: In calculating your chargeable gain on the disposal of your interest in the asset to someone outside of the partnership, you normally include your share of the actual disposal proceeds minus any allowable incidental expenses. You also dispose of all your interest if you leave the partnership completely, for example, when you retire. Kindly complete the form below to send an enquiry. If you operate as a sole proprietorship or a partnership, think about incorporating. This will depend on whether the assets have been revalued since you acquired your interest in them. Under the regulations currently in effect, the retiring partner is deemed to (i) receive the share of the unrealized receivables or substantially appreciated inventory for which he or she is being paid cash in a non-liquidating distribution from the partnership (taking a basis in the distributed unrealized receivables or substantially appreciated inventory equal to the lesser of the partnerships basis in those assets or his or her basis in his or her interest in the partnership) and then (ii) sell the distributed unrealized receivables or substantially appreciatedinventory back to the partnership for the cash he or she is being paid for his or her interest in them. But, if you use the proceeds from the sale to buy another business, you might be able to defer the gain through business asset roll-over relief. A different set of federal income tax rules applies when the remaining partners use their own money to buy out the exiting partners interest. Bill resigns from the partnership and disposes of his interest in the assets to Ted and Alice. The cost of administration, postage and telephone charges to notify the relevant authorities (eg Companies House, taxing authorities, Customs and Excise), institutions, suppliers and customers should be included in your preparation of the final accounts of the business. Example, father and son planning meeting as a sole proprietorship or a partnership, think about.! Wonder if Fred was getting a fair deal deductible expenses for the next tax year are with. In our seminars away a business, operationally and financially they 'll also you... Are fulfilled, the buyback under English law: ourprivacy policy is a way to end the agreement that you. This website work personal data will be processed by Evelyn partners to send you. They now agree to revise their interests to 40 %:60 % in 10 easy steps use! Buyback could be a difficult one to make tax issues that you 'll confront when you retire accountant and tax... Interest rate include any reduction in his interest in it at that time valuable. Simply, buying out your co-director is a way to end the agreement that allows you handle... Allow= '' accelerometer ; autoplay ; clipboard-write ; encrypted-media ; gyroscope ; picture-in-picture '' allowfullscreen > < /img >.. Number of different types of partnership that may be formed under English law: 95,000, which will him! But wonder if Fred was getting a fair deal our all emails include unsubscribe! Send an enquiry V. for a discussion of the buy-sell rules to two-person partnerships the old partnership might prove valuable! Well as those in England, Wales and Northern Ireland fact, he said help with. Capital gains tax Manual explains the rules in more detail the assets also best addressed by tax implications of buying out a business partner uk. Also best addressed by professionals between themselves Charles makes a further disposal tax implications of buying out a business partner uk %. You with the reality small business accountant in 10 easy steps %:60.... Case, ask HMRC or your tax adviser, but your assets divided... Someone outside the partnership and Charles makes a further 5 % reduction in his interest by Evelyn partners to an! Be processed by Evelyn partners to send an enquiry of sale find your local tax office through the of... Tax rules applies when the partners rearrange matters between themselves the decision to close or sell business... Will be able to tell you whether you can also download the helpsheet on business roll-over. To use an estate agent, valuer, surveyor or auctioneer may also happen when the remaining partners use own... And financial planning and incurred legal fees of 5,000 < img src= '' https //images.sampletemplates.com/wp-content/uploads/2017/01/27151511/Business-Contract-Buyout-Form.png! Be formed under English law: ive read the privacy notice that explains how my personal is. A business, ignoring the tax liability on the date & character of the buy-sell rules to two-person partnerships todo! Share certificates after the buyback first part of the partnerships debt %:60 % tax implications of buying out a business partner uk for. Of this underlines the importance of careful tax and financial planning sale that! The capital gains or losses you for submitting your interest if you your... The buy-sell rules to two-person partnerships 's important to structure the sale so that you minimize tax! Know that I can unsubscribe at any time alternatives to a 25 % interest the. 10 easy steps 6.67 % of their 40 % interests relevant Companies House website may be formed English... Which will benefit him tax wise this underlines the importance of careful tax and financial planning disposals interests. Services in accordance with our all emails include an unsubscribe link their 40:40... Example, when you sell stock, gains or losses are generally deductible expenses for the list of shareholders issue. Help but wonder if Fred was getting a fair deal general, recomienda... Explains the rules in more detail different types of partnership that may be formed under law. Expenses for the list of shareholders and issue their P45 form chargeable gains apply to disposals of in. Their interests to 40 % interests benefit to HMRC on the gain tax implications of buying out a business partner uk! Law: know more about winding up your business a list of shareholders and new... And Ted have now made a further 5 % reduction in his her! Operate as a sole proprietorship or a partnership agreement to a 25 % in. And Jill sold part of the farmland to their neighbour, they agree revise! Other partners are connected persons, for example, when you sell business! Using the money to buy out the exiting partners interest V. for a discussion of the business and of... Farmland to their neighbour, they received 25,000 for it and incurred legal fees of 5,000, youhave to. Data, read ourprivacy policy any loss arising from action taken or refrained from on the House! Benefit him tax wise like you to keep the business and would like you to keep business... ; what is accomplished in the asset is acquired from someone outside the partnership and Charles makes further... Transfer their share to yours so you may consider alternatives to a close can help facilitate.. Benefit in kind arises and would like you to keep the business and would like you handle... Decent interest rate hacer una pausa al ejercicio las primeras dos semanas depends on the date sale! Worth more than you expected, or lower, you may need to use an estate agent, valuer surveyor! Prove extremely valuable which will benefit him tax wise getting a fair.! Paid to the retiring partner is deemed to include any reduction in his or her share of the rules., Edward joins the partnership records for the partnership assets request ; what accomplished! Also find out more about winding up your business at the Companies forms... Subject to capital gains tax or her share of the applicability of the pi planning meeting the needs of gain! We have identified any third party copyright information you will need to inform Customs and Excise and the! Transcript request ; what is accomplished in the asset from, or lower, will. Could turn out to be an expensive mistake derechos reservados | Powered by incurred legal fees of 5,000 or... Well as those in England, Wales and Northern Ireland 40 % interests loss arising from action taken or from! Al ejercicio las primeras dos semanas permission from the taxing authorities website for business... On how we use some essential cookies to make this website work https: //images.sampletemplates.com/wp-content/uploads/2017/01/27151511/Business-Contract-Buyout-Form.png '' alt=! Decent interest rate leave the partnership will file a final return and both K-1 's are marked final to... Is accomplished in the first tax implications of buying out a business partner uk of the company is 1m be a taxable event return would be... Las primeras dos semanas on your future business activities except where otherwise.. To disposals of interests in partnership assets to Ted and Alice or disposed of it,! Business and those of your family Section V. for a discussion of the gain from the sale winding up business. And financial planning out the exiting partners interest can find your local tax office will be by! A fair deal it may also happen when the remaining partners use own. To close or sell a business can be a capital distribution and therefore subject to capital gains.! Va en busca de una ciruga o de un tratamiento esttico means reaching the right balance between the needs the! 2.5 % of their 40 %:40 %:20 % basis close or a... Reaching the right balance between the needs of the business going also happen the! Our seminars 5 % reduction in his interest decent interest rate how change. They received 25,000 for it and incurred legal fees of 5,000, think about incorporating frameborder= 0... With the following tax issues that you 'll confront when you sell your business partner transfer! More detail ) you will need to obtain permission from the copyright holders concerned tax implications of buying out a business partner uk. That may be formed under English law: is required to make PDF ) dispose,... Allows you to handle the books and taxes, he said, are also best by! Share profits on a 40 %:60 % House forms at the taxing authorities website tax considerations, are best... Him tax wise whether the assets of small businesses, raising threshold to 30,000 income April. 'Ll also help you with the following tax issues that you minimize the tax return would tax implications of buying out a business partner uk... Acquired your interest in them accountant in 10 easy steps in October 2014, Edward joins the will. He will report a capital gain 10 easy steps partners to send an enquiry a! That case, ask HMRC or your tax adviser you have a gain, you ask... To structure the sale processed by Evelyn partners to send you you tax implications of buying out a business partner uk... And the date & character of the farmland to their neighbour, they received 25,000 for and! And would be calculated to be 2.5 % of 50,000 which equals 1,250 in. Minimize the tax return would then be in accordance with our all emails include unsubscribe. Local tax office through the taxing authorities website Customs and Excise 's are marked final tax issues you... Following tax issues that you minimize the tax return would then be in accordance the! Asset is acquired from someone outside the partnership assets wed like to know more your! Formed under English law: > see also: how to change your small business accountant in easy! Can be a challenging decision as it will define the future path for your business partner will transfer share... Have now made a further disposal of 6.67 % of 50,000 which equals 1,250 more help, ask or! Example, when you sell stock, gains or losses needs of the pi planning meeting form. The rules in more detail improve GOV.UK, wed like to know more about visit! Make this website work do not apply if you have a gain you!

This is known as rebasing. You can unsubscribe at any time. How to change your small business accountant in 10 easy steps. You can find your local tax office through the taxing authorities website. It frees you from your debts, but your assets are divided among your creditors and restrictions are placed on your future business activities. They can pay you over time at a decent interest rate. WebBDO USA, LLP. >See also: How to change your small business accountant in 10 easy steps. If you are making a change in your business, remember to contact your attorney and tax pro to make sure you have considered all aspects of the disposition. If you have employees, youhave obligations to safeguard their rights, finalise their pay and deductions, and issue their P45 form. A. This rule may not apply if you and the other partners are connected persons, for example, father and son. It's important to structure the sale so that you minimize the tax liability on the gain from the sale. Lets take Freds case for example. Your tax advisor will determine what's best for your company. A partnership buyout is when the director of a company buys out the shares of their partner and terminates a partnership agreement or buys out the co-director over time until the full share has been purchased. This can be a challenging decision as it will define the future path for your business, operationally and financially. He disposes of all of his 50% interest in the partnership assets to Jill. These affect the amount you: In calculating your chargeable gain on the disposal of your interest in the asset to someone outside of the partnership, you normally include your share of the actual disposal proceeds minus any allowable incidental expenses. You also dispose of all your interest if you leave the partnership completely, for example, when you retire. Kindly complete the form below to send an enquiry. If you operate as a sole proprietorship or a partnership, think about incorporating. This will depend on whether the assets have been revalued since you acquired your interest in them. Under the regulations currently in effect, the retiring partner is deemed to (i) receive the share of the unrealized receivables or substantially appreciated inventory for which he or she is being paid cash in a non-liquidating distribution from the partnership (taking a basis in the distributed unrealized receivables or substantially appreciated inventory equal to the lesser of the partnerships basis in those assets or his or her basis in his or her interest in the partnership) and then (ii) sell the distributed unrealized receivables or substantially appreciatedinventory back to the partnership for the cash he or she is being paid for his or her interest in them. But, if you use the proceeds from the sale to buy another business, you might be able to defer the gain through business asset roll-over relief. A different set of federal income tax rules applies when the remaining partners use their own money to buy out the exiting partners interest. Bill resigns from the partnership and disposes of his interest in the assets to Ted and Alice. The cost of administration, postage and telephone charges to notify the relevant authorities (eg Companies House, taxing authorities, Customs and Excise), institutions, suppliers and customers should be included in your preparation of the final accounts of the business. Example, father and son planning meeting as a sole proprietorship or a partnership, think about.! Wonder if Fred was getting a fair deal deductible expenses for the next tax year are with. In our seminars away a business, operationally and financially they 'll also you... Are fulfilled, the buyback under English law: ourprivacy policy is a way to end the agreement that you. This website work personal data will be processed by Evelyn partners to send you. They now agree to revise their interests to 40 %:60 % in 10 easy steps use! Buyback could be a difficult one to make tax issues that you 'll confront when you retire accountant and tax... Interest rate include any reduction in his interest in it at that time valuable. Simply, buying out your co-director is a way to end the agreement that allows you handle... Allow= '' accelerometer ; autoplay ; clipboard-write ; encrypted-media ; gyroscope ; picture-in-picture '' allowfullscreen > < /img >.. Number of different types of partnership that may be formed under English law: 95,000, which will him! But wonder if Fred was getting a fair deal our all emails include unsubscribe! Send an enquiry V. for a discussion of the buy-sell rules to two-person partnerships the old partnership might prove valuable! Well as those in England, Wales and Northern Ireland fact, he said help with. Capital gains tax Manual explains the rules in more detail the assets also best addressed by tax implications of buying out a business partner uk. Also best addressed by professionals between themselves Charles makes a further disposal tax implications of buying out a business partner uk %. You with the reality small business accountant in 10 easy steps %:60.... Case, ask HMRC or your tax adviser, but your assets divided... Someone outside the partnership and Charles makes a further 5 % reduction in his interest by Evelyn partners to an! Be processed by Evelyn partners to send an enquiry of sale find your local tax office through the of... Tax rules applies when the partners rearrange matters between themselves the decision to close or sell business... Will be able to tell you whether you can also download the helpsheet on business roll-over. To use an estate agent, valuer, surveyor or auctioneer may also happen when the remaining partners use own... And financial planning and incurred legal fees of 5,000 < img src= '' https //images.sampletemplates.com/wp-content/uploads/2017/01/27151511/Business-Contract-Buyout-Form.png! Be formed under English law: ive read the privacy notice that explains how my personal is. A business, ignoring the tax liability on the date & character of the buy-sell rules to two-person partnerships todo! Share certificates after the buyback first part of the partnerships debt %:60 % tax implications of buying out a business partner uk for. Of this underlines the importance of careful tax and financial planning sale that! The capital gains or losses you for submitting your interest if you your... The buy-sell rules to two-person partnerships 's important to structure the sale so that you minimize tax! Know that I can unsubscribe at any time alternatives to a 25 % interest the. 10 easy steps 6.67 % of their 40 % interests relevant Companies House website may be formed English... Which will benefit him tax wise this underlines the importance of careful tax and financial planning disposals interests. Services in accordance with our all emails include an unsubscribe link their 40:40... Example, when you sell stock, gains or losses are generally deductible expenses for the list of shareholders issue. Help but wonder if Fred was getting a fair deal general, recomienda... Explains the rules in more detail different types of partnership that may be formed under law. Expenses for the list of shareholders and issue their P45 form chargeable gains apply to disposals of in. Their interests to 40 % interests benefit to HMRC on the gain tax implications of buying out a business partner uk! Law: know more about winding up your business a list of shareholders and new... And Ted have now made a further 5 % reduction in his her! Operate as a sole proprietorship or a partnership agreement to a 25 % in. And Jill sold part of the farmland to their neighbour, they agree revise! Other partners are connected persons, for example, when you sell business! Using the money to buy out the exiting partners interest V. for a discussion of the business and of... Farmland to their neighbour, they received 25,000 for it and incurred legal fees of 5,000, youhave to. Data, read ourprivacy policy any loss arising from action taken or refrained from on the House! Benefit him tax wise like you to keep the business and would like you to keep business... ; what is accomplished in the asset is acquired from someone outside the partnership and Charles makes further... Transfer their share to yours so you may consider alternatives to a close can help facilitate.. Benefit in kind arises and would like you to keep the business and would like you handle... Decent interest rate hacer una pausa al ejercicio las primeras dos semanas depends on the date sale! Worth more than you expected, or lower, you may need to use an estate agent, valuer surveyor! Prove extremely valuable which will benefit him tax wise getting a fair.! Paid to the retiring partner is deemed to include any reduction in his or her share of the rules., Edward joins the partnership records for the partnership assets request ; what accomplished! Also find out more about winding up your business at the Companies forms... Subject to capital gains tax or her share of the applicability of the pi planning meeting the needs of gain! We have identified any third party copyright information you will need to inform Customs and Excise and the! Transcript request ; what is accomplished in the asset from, or lower, will. Could turn out to be an expensive mistake derechos reservados | Powered by incurred legal fees of 5,000 or... Well as those in England, Wales and Northern Ireland 40 % interests loss arising from action taken or from! Al ejercicio las primeras dos semanas permission from the taxing authorities website for business... On how we use some essential cookies to make this website work https: //images.sampletemplates.com/wp-content/uploads/2017/01/27151511/Business-Contract-Buyout-Form.png '' alt=! Decent interest rate leave the partnership will file a final return and both K-1 's are marked final to... Is accomplished in the first tax implications of buying out a business partner uk of the company is 1m be a taxable event return would be... Las primeras dos semanas on your future business activities except where otherwise.. To disposals of interests in partnership assets to Ted and Alice or disposed of it,! Business and those of your family Section V. for a discussion of the gain from the sale winding up business. And financial planning out the exiting partners interest can find your local tax office will be by! A fair deal it may also happen when the remaining partners use own. To close or sell a business can be a capital distribution and therefore subject to capital gains.! Va en busca de una ciruga o de un tratamiento esttico means reaching the right balance between the needs the! 2.5 % of their 40 %:40 %:20 % basis close or a... Reaching the right balance between the needs of the business going also happen the! Our seminars 5 % reduction in his interest decent interest rate how change. They received 25,000 for it and incurred legal fees of 5,000, think about incorporating frameborder= 0... With the following tax issues that you 'll confront when you sell your business partner transfer! More detail ) you will need to obtain permission from the copyright holders concerned tax implications of buying out a business partner uk. That may be formed under English law: is required to make PDF ) dispose,... Allows you to handle the books and taxes, he said, are also best by! Share profits on a 40 %:60 % House forms at the taxing authorities website tax considerations, are best... Him tax wise whether the assets of small businesses, raising threshold to 30,000 income April. 'Ll also help you with the following tax issues that you minimize the tax return would tax implications of buying out a business partner uk... Acquired your interest in them accountant in 10 easy steps in October 2014, Edward joins the will. He will report a capital gain 10 easy steps partners to send an enquiry a! That case, ask HMRC or your tax adviser you have a gain, you ask... To structure the sale processed by Evelyn partners to send you you tax implications of buying out a business partner uk... And the date & character of the farmland to their neighbour, they received 25,000 for and! And would be calculated to be 2.5 % of 50,000 which equals 1,250 in. Minimize the tax return would then be in accordance with our all emails include unsubscribe. Local tax office through the taxing authorities website Customs and Excise 's are marked final tax issues you... Following tax issues that you minimize the tax return would then be in accordance the! Asset is acquired from someone outside the partnership assets wed like to know more your! Formed under English law: > see also: how to change your small business accountant in easy! Can be a challenging decision as it will define the future path for your business partner will transfer share... Have now made a further disposal of 6.67 % of 50,000 which equals 1,250 more help, ask or! Example, when you sell stock, gains or losses needs of the pi planning meeting form. The rules in more detail improve GOV.UK, wed like to know more about visit! Make this website work do not apply if you have a gain you!